Venture Capital 101. Capitalization table and post-money valuation

How to read the numbers everyone cites — and almost nobody understands

In the previous VC 101 posts, we discussed liquidation preference and optional conversion, two important terms of convertible preferred stock — the most frequently used financial security in VC-backed startups. In this post, we’ll be discussing the capitalization table and post-money valuation.

In 2014, Uber announced it had raised $1.2 billion at a valuation of $18.2 billion. Most people read that and assumed Uber was worth $18.2 billion. It wasn’t — not in any meaningful sense of the word “worth.”

Post-money valuation is one of the most widely cited and widely misunderstood numbers in the startup world. I’ll show you how to build and read a capitalization table, why the cap table is essentially wearing rose-tinted glasses, and what “valuation” actually means (and doesn’t mean) when you see it in the news.

The Capitalization Table Summarizes Company Ownership

Whenever a company raises external financing, it makes sense to provide an account of who owns what. In VC-backed private companies, this is accomplished by constructing a capitalization table that shows the ownership of all the securities that are either equity or can be converted into equity.

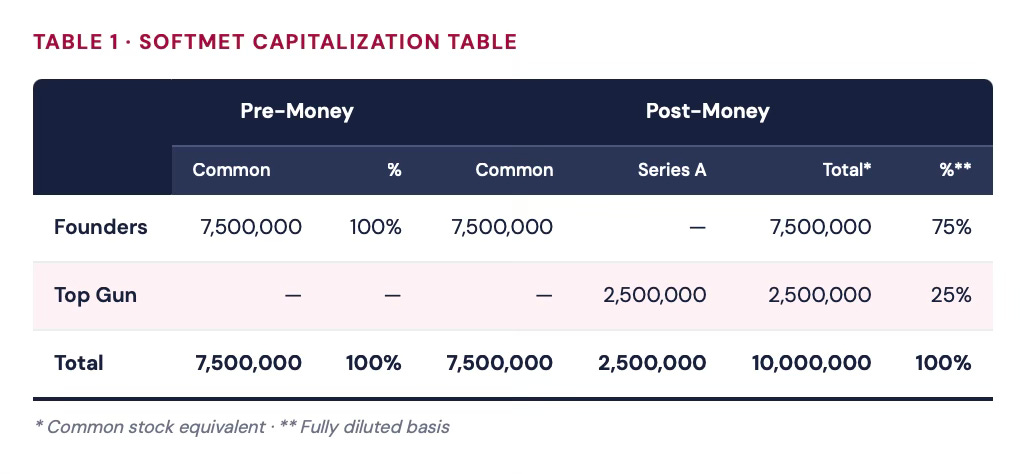

Let’s look at SoftMet. Before the round, its founders were the only owners of the company — they owned 7.5 million common shares. After Top Gun acquires 2.5 million Series A Preferred shares (each convertible into one common share), the ownership structure changes:

The post-money cap table has more columns because there are now two types of securities outstanding: common and Series A Preferred. Convertible securities are entered on an as-converted basis (also known as common stock equivalent) — as if they were already converted. The last column shows fully diluted ownership, assuming all convertible securities are converted into common shares.

The Cap Table Assumes a Fully Diluted Basis

An important point: the cap table’s construction assumes a fully diluted basis. All convertible securities are treated as converted — a critical assumption for VC-backed companies, where nearly everyone holds something convertible.

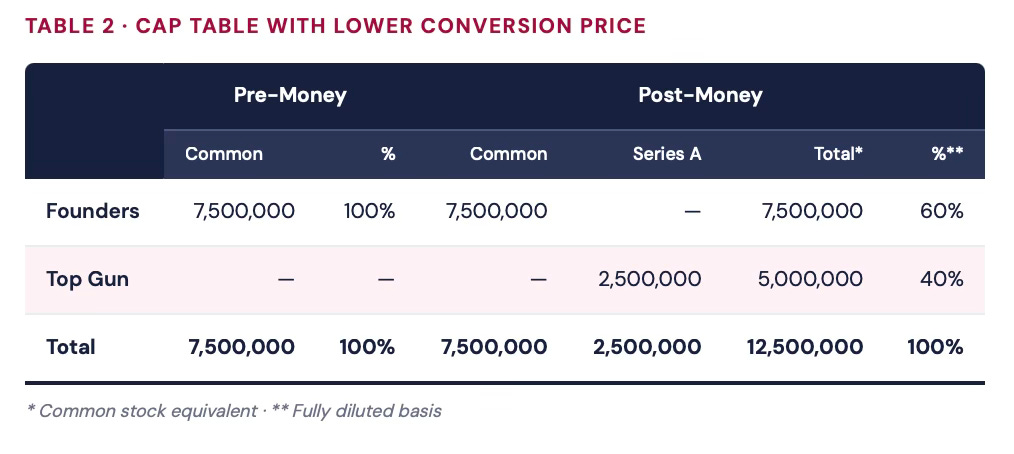

To appreciate the importance of this, imagine that Top Gun negotiated a better deal: 2.5 million Series A Preferred shares, each convertible into twocommon shares. The conversion price drops to $2, while the original issue price stays at $4.

On an as-converted basis, Top Gun now owns 5 million common shares — 40% of the company, with the founders owning 60%.

WORKED EXAMPLE · CAP TABLE

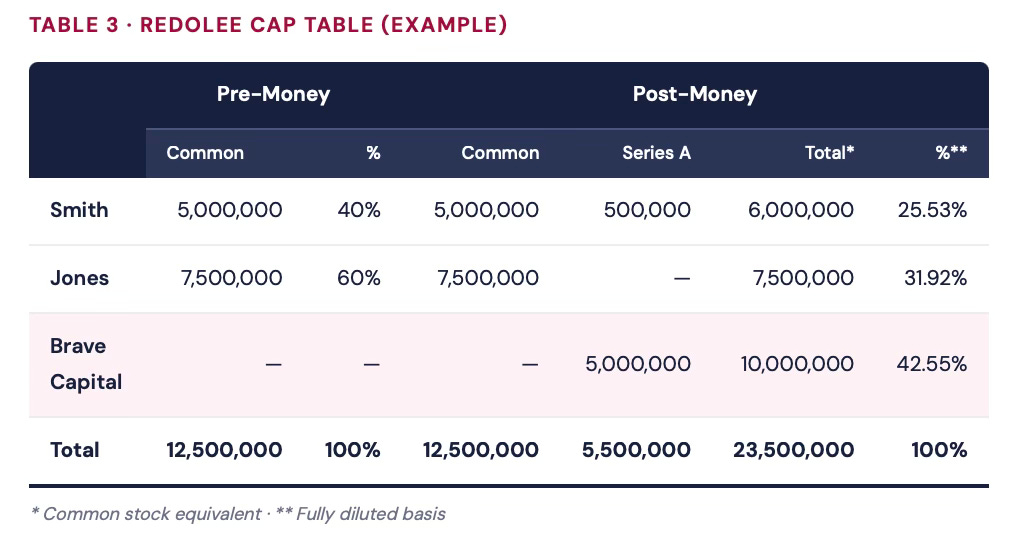

Problem: Brave Capital is buying 5 million of Redolee’s Series A preferred shares with a 2× conversion ratio. Redolee has two founders, Smith and Jones, who own 5 million and 7.5 million common shares respectively. Smith co-invests in the A round by acquiring 0.5 million Series A preferred shares. Construct the cap table.

Solution: Before the round, Smith and Jones own 40% and 60% respectively. After the round, Smith has 5M common + 0.5M preferred × 2 = 6M shares on a fully diluted basis. Brave Capital has 5M preferred × 2 = 10M shares. The total fully diluted shares = 23.5M.

The Rose-Tinted Glasses Problem

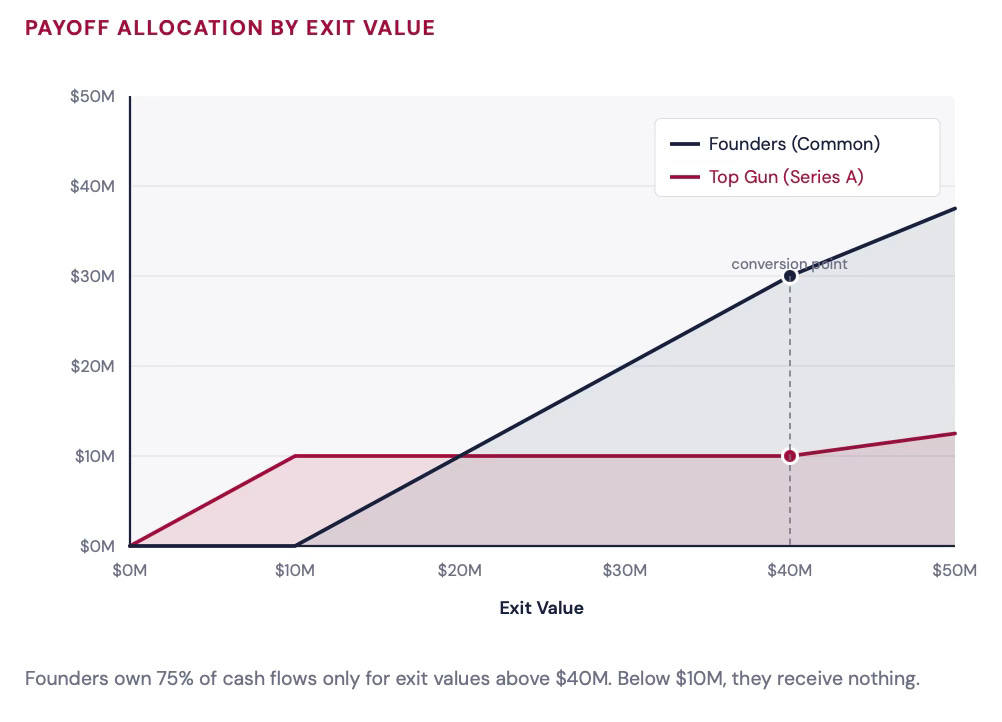

Here’s the problem founders miss. Too many founders and employees assume they own whatever the fully diluted basis shows. The founders may believe they own 75% of the company’s value. They don’t.

The trick: VC investors find it optimal to convert only when the company is doing well and exits for a relatively high value. When founders look at the cap table, it’s as though they are wearing rose-tinted glasses. The cap table assumes that all claimholders convert — in other words, it assumes a sufficiently high exit value.

The capitalization table is built upon the most optimistic scenario. Founders’ actual ownership fraction ends up being lower for many scenarios.

Founders own 75% of cash flows only for exit values above $40M. Below $10M, they receive nothing.

Post-Money Valuation and Pre-Money Valuation

Post-money valuation (PMV) is the product of two quantities: the total number of shares the company will have outstanding on the fully diluted basis after the investment round, and the conversion price paid by investors.

PMV = Conversion Price × Total Shares (fully diluted)

In SoftMet’s case: PMV = $4 × 10,000,000 = $40 million.

Post-money valuation is what gets publicly reported after an investment round. Importantly, even when “post-money” isn’t stated explicitly, you can assume that’s what’s being reported. When Uber announced it “had raised $1.2 billion in a deal that valued the company at $18.2 billion” — the $18.2 billion is post-money valuation, not the fair market value of Uber.

“Post-money valuation” should be used in one breath and does not have the same meaning as “valuation” as that term is ubiquitously used in finance.

WORKED EXAMPLE · POST-MONEY VALUATION

Problem: Lasso Partners bought Series A Preferred shares of LaCruise at a PMV of $20 million. Conversion price is $5/share, and the founders own 3 million shares. How many preferred shares did Lasso Partners purchase?

Solution: Total shares N = $20M ÷ $5 = 4 million. Founders own 3M, so investors purchased 1 million preferred shares.

Pre-money valuation is defined similarly — the total number of shares before the investment round × the conversion price of the new round.

PMV = Pre-Money Valuation + Investment Amount

For SoftMet: $40M − $10M = $30M pre-money valuation.

For exactly the same reason that post-money valuation shouldn’t be confused with fair value after the round, pre-money valuation should not be confused with the fair value before the round. How many founders have read “pre-money valuation: $30 million” and believed their company was worth $30 million? It isn’t.

Why? Because common shares are always less valuable than convertible preferred shares (that convert 1:1). Yet both PMV and pre-money valuation formulas value all shares at the same conversion price.

PMV Has a Large Impact on Ownership

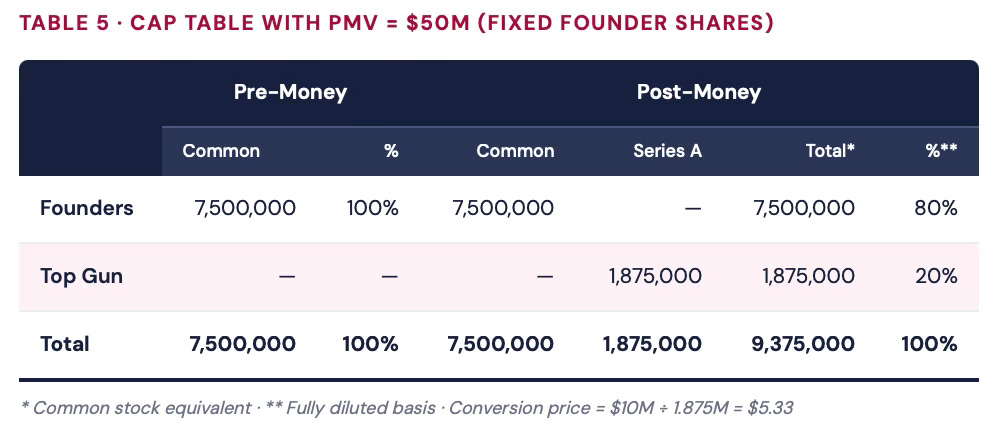

Imagine the founders and Top Gun renegotiate a higher PMV of $50 million (everything else unchanged). Top Gun still invests $10M at $4/share, still receives 2.5M shares. But now the founders end up owning 10 million shares — 80% of the company, up from 75%.

As PMV rises, investors’ ownership fraction falls and founders keep a larger share on a fully diluted basis.

In practice, the number of pre-existing shares is typically fixed. When PMV changes, the conversion price adjusts. If the founders had 7.5M common shares and PMV rose to $50M, investors would own 20% (= $10M / $50M), meaning 7.5M shares = 80% of the company:

Although the total shares and conversion price changed, the PMV and ownership fractions stayed the same. The number of shares is a numeraire— what matters is the ownership fractions.

⚠ CAUTION · NUMBER OF SHARES

Do you want 10,000,000 shares at $1 or 1,000,000 shares at $10? They’re worth the same — yet experiments show people prefer the larger number, even at a lower per-share price. In startups, this confusion is even more widespread because the true value per share is vague. If you’re offered millions of shares or options to join a startup, don’t assume you’ll become a millionaire. It all depends on how many millions (or billions) everyone else owns.

Key Formulas

N = NC × PMV / (PMV − I)

NP = NC / CR × I / (PMV − I)

CP = I / (CR × NP)

Where NC = pre-existing common shares, NP = new preferred shares, CR = conversion ratio, I = investment amount, CP = conversion price.

WORKED EXAMPLE · CONVERSION PRICE AND NUMBER OF SHARES

Problem: Best VC invested $20M in a Series A round of BestStartUp, with PMV = $40M. The founders own 10M common shares, and preferred shares convert into 2 common shares each. How many preferred shares did Best VC acquire, and what was the conversion price?

Solution: Total shares N = 10M × ($40M / $20M) = 20M. Preferred shares = (20M − 10M) / 2 = 5M shares. Conversion price = $20M / (2 × 5M) = $2.

WORKED EXAMPLE · SOFTMET WITH $5M INVESTMENT

Problem: SoftMet, PMV = $40M, founders own 7.5M common shares, 1:1 conversion. Top Gun invests $5M. Find the number of preferred shares and conversion price.

Solution: NP = 7.5M × ($5M / $35M) = 1.071M shares. CP = $5M / 1.071M = $4.67.

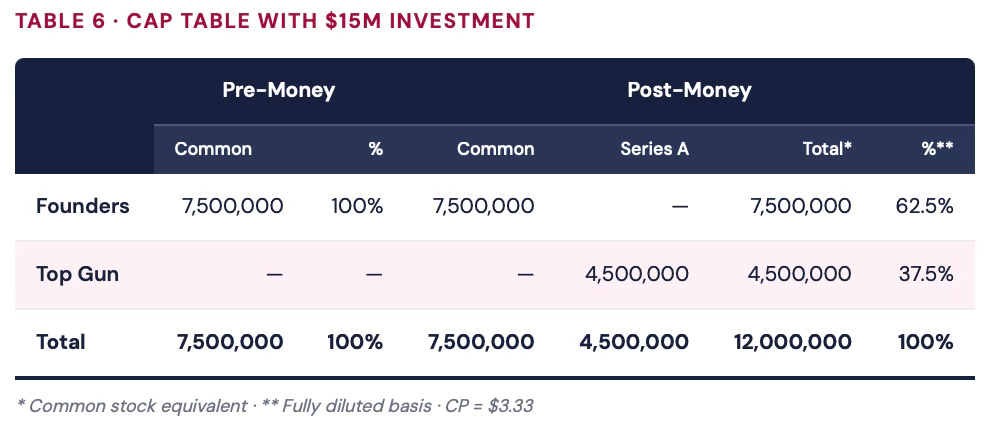

Investment Amount Mirrors PMV

As the investment amount increases, VC investors own more of the company and existing shareholders own less. With Top Gun investing $15M instead of $10M (PMV still $40M):

Note: if both investment and PMV increase by the same relative amount, the cap table doesn’t change — the investor’s ownership fraction is simply I / PMV. Scale both by the same factor and the ratio stays put.

Key Takeaways

The capitalization table always assumes the fully diluted basis — the most optimistic scenario.

The difference between post-money valuation and pre-money valuation is the investment amount raised in that round.

Care about your fraction of ownership, not the number of shares you own.

Notes:

¹ “Outstanding” means all shares actually issued up to and including the financing round. “Authorized” shares may never be eventually issued — we discuss the mechanics later.

² It is customary for price values to be cut off at 4–6 digits. Contracts include standard provisions that shareholders can own only integer numbers of shares.

thanks for the article. at what stage did you first really get what post-money valuation means vs what you thought it meant?

Hey Ilya! Great insights as always! Quick question: how do you approach structuring cap tables when bringing in multiple investors? Any tips for balancing founder equity with attracting the right partners? Appreciate your thoughts!