Venture Capital 101. Introduction

What every founder and investor should know

TLDR: Opening the Stanford VC class insights to everybody. In this post, we’ll be learning how cash flow terms work, how liquidation preferences affect your payout, how convertible preferred stock gives investors the upper hand — basics startup founders should know.

Welcome and my motivation

I have been teaching the Venture Capital course at the Stanford Graduate School of Business for many years. In this time, 1,300+ students took the class, ~500 went on to found startups, ~600 went to work in the venture capital (VC) and more broadly private equity industry as investors. I stay in touch with many of my students and often get emails or messages from them saying that they were raising a round or negotiating a term sheet and once again “dusted off the teaching notes and slides from your class, Professor.”

I always wanted to share my knowledge and experience broadly, especially because the world of VC and startups is so often veiled in secrecy and misunderstood. This is why I started posting, almost daily, the results of my VC research on LinkedIn. But sharing the details of a complex and challenging course, where ideas build on other ideas, requires a different medium. And so, here I am.

After working on each article you should learn a great deal about the ways investors make decisions, entrepreneurs and investors negotiate with other on the allocation of cash flows and corporate governance, and myriads of other stuff that are used day in and day out in the startup world.

In the first several articles we will go straight into the heat of the matter and talk mostly about cash flow terms in the first VC round. Cash flow terms are basically rules on who gets what when it is time to divide the spoils. We will meet the most common financial security used in venture capital financing, convertible preferred stock. We will cover all the main contractual terms that determine the allocation of payoffs to entrepreneurs and investors. Once we cover the first VC round, we will proceed with covering follow-on VC rounds. Only then we will be ready to cover pre-VC rounds, including such wonderful securities as SAFEs and convertible notes. Many students are asking me, why on earth can’t we start with SAFEs – after all, this is the first security many founders issue these days. But the critical feature of a SAFE is its conversion into the security the startup will issue later on, and without knowing that security it is tough to understand SAFE properly. Once we cover the cash flow terms, we will discuss control rights, corporate governance, and conflicts of interest in startups. These are absolutely critical discussion points. As I tell my students again and again, “you can lose control in your startup only once. Once lost, it is lost forever.”

Stylized example

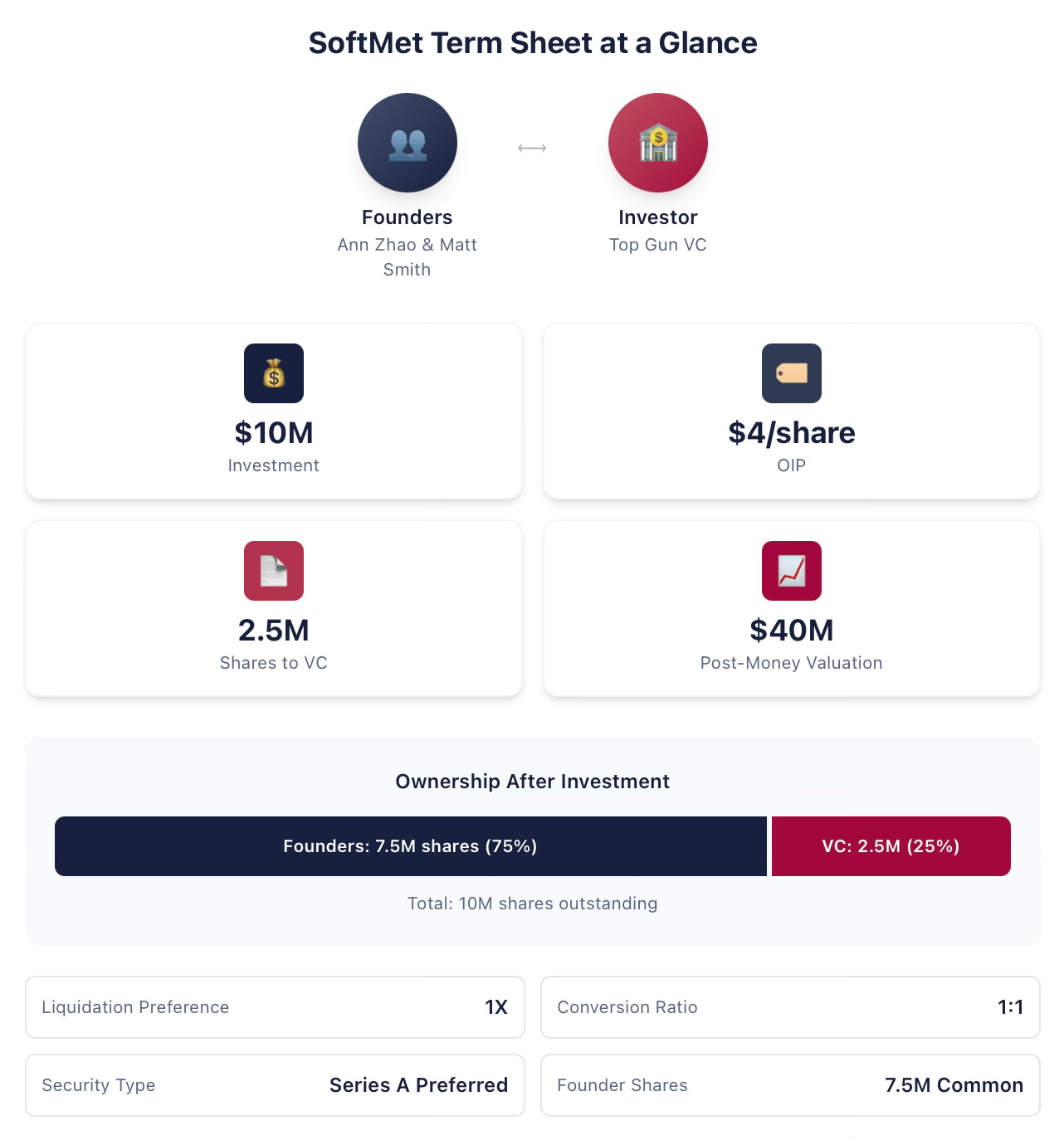

I will use one stylized example as we go through the cash flow topics, and will modify and expand it as more stuff is added. Ann Zhao and Matt Smith are co-founders of SoftMet, a technology startup. During their fundraising journey, they met with Rob Arnott, a partner at Top Gun, a venture capital (VC) firm. Rob then invited Ann and Matt to present the startup idea to the entire Top Gun’s partnership. A week later, the founders received a term sheet from Top Gun. The term sheet proposes that:

Top Gun invests $10 million into SoftMet.

Top Gun receives SoftMet’s Series A Preferred stock that will be issued at the original issue price of $4.

Series A Preferred stock has liquidation preference of 1X.

One Series A Preferred share can convert into one common share of SoftMet.

Series A Preferred stock comes with various additional terms and conditions.

Founders own 7.5 million shares of common stock.

The post-money valuation of the company is $40 million.

Ann and Matt need to understand the implications of this term sheet: What exactly is Series A Preferred stock? What is post-money valuation? What is liquidation preference? What is conversion? What features of this proposal should they pay particular attention to? Of all the terms, which ones might have important financial implications that they may want to renegotiate? What are more founder-friendly terms?

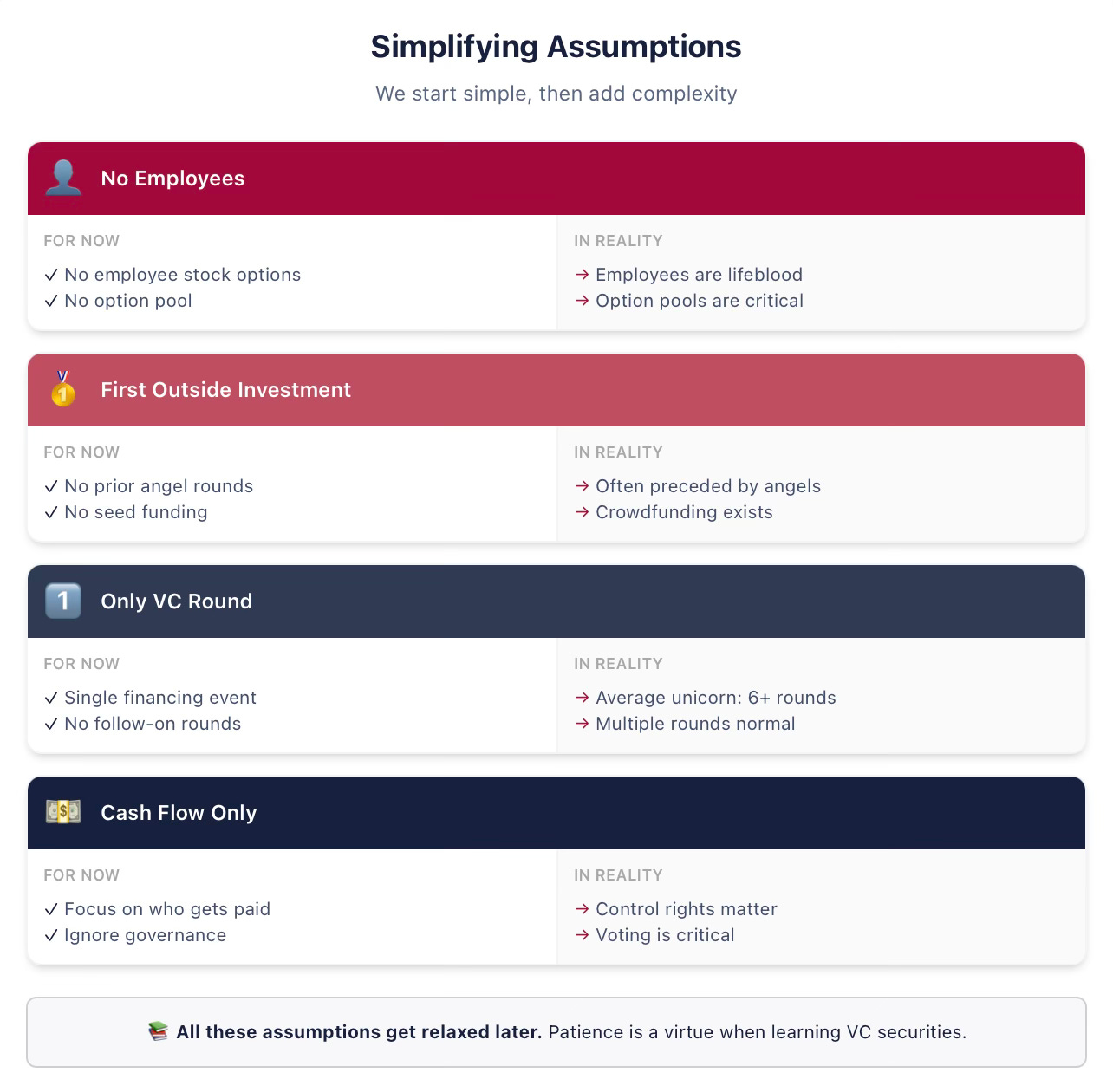

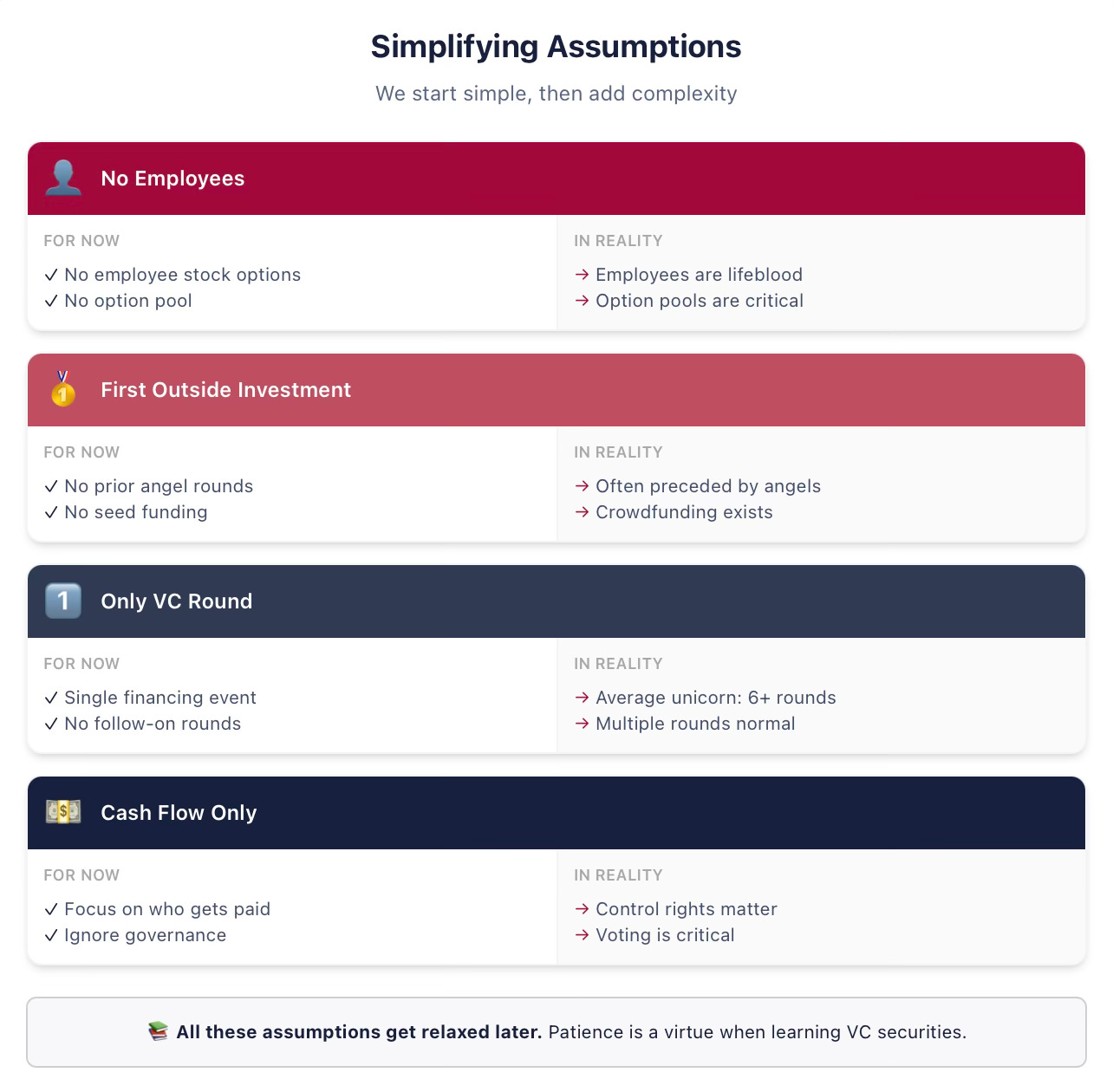

We need to make some simplifying assumptions to introduce all the concepts

To keep things clear, we’ll start with some simplifying assumptions. We will relax all our temporary assumptions in subsequent notes, so stay tuned! And do not walk away because you think that this Ivory tower professor does not know that founders don’t “own shares” but rather “vest,” etc. I know and we will get back to all of this, in due time.

It is useful to summarize what I will be assuming throughout the first series of notes about the first VC round (and if the terms below are not familiar, this is exactly why we simplify for now!):

Assumption: SoftMet does not hire any employees. This assumption implies that SoftMet does not need to compensate employees with cash or stock. It also means we treat founders purely as owners, not employees. I will discuss vesting and founder employment terms later!

Assumption: Top Gun is the first outside investor in SoftMet. In reality, most VC rounds are preceded by angel or seed financing with different securities.

Assumption: This financing round will be the only investment SoftMet ever raises as a private VC-backed company. In reality, my research shows that an average unicorn in the US raises more than six VC rounds. We certainly relax this assumption sooner than later.

Assumption: Only cash flow terms matter. Term sheets also cover corporate governance — control rights, voting, board seats — but we’ll tackle those later.

Investors Get Financial Securities in Return for Their Investment

Top Gun’s $10 million investment is a venture round — cash in exchange for securities. The $10 million that Top Gun proposes to invest is known as the investment amount.

In return for its investment, Top Gun will acquire securities that give it partial ownership of SoftMet. Specifically, certain number of shares of the new security, Series A Preferred stock, would be issued as a part of the round and given to Top Gun. But how many shares will Top Gun receive? What is the ownership split after Top Gun invests? And how will any future proceeds be shared between the founders and the VC investors?

The term sheet provides clues to answering these questions by specifying who gets what in different scenarios. The number of shares Top Gun acquires is determined by the investment amount and the original issue price of the Series A Preferred stock. Original issue price is the price of one share paid by investor at the time of issuance. It is commonly abbreviated as OIP. Original issue price also can be called Original purchase price (OPP).

CAUTION

OIP vs Par Value

The Original Issue Price (OIP) should not be confused with the par value. The par value of a share of stock is the value of the share as stated in the corporate charter. The par value is arbitrarily chosen at the time of filing and has little bearing on actual company valuation. It really has no practically relevant economic meaning. The specific par values are typically $0.001 or $0.0001. “No par” also can be used.

We can use OIP to determine the number of shares that Top Gun acquires. The investment amount is $10 million and the OIP is $4. Top Gun receives the quotient of the two:

Thus, Top Gun receives 2.5 million shares of Series A Preferred stock in exchange for a $10 million cash investment in SoftMet. More generally, the relationship between OIP, investment amount, and the number of shares the investor in this round receives is:

Once you know two of the three quantities in Equation , you can determine the third. Real-world term sheets differ quite a bit in how exactly they describe the proposed investment, but it should always be possible to back out all the three quantities from information that is given. SoftMet’s term sheet gives the investment amount and OIP. Alternatively, term sheets may give the investment amount and the number of shares that investors receive.

Example 1. Original issue price

Problem

VC fund Great Innovation Partners invested in an early-stage company Fox Solutions, Inc. For the investment amount of $25 million the fund received 2 million shares of Series Seed Preferred stock. What is the original issue price of this security?

Solution

The original issue price is

In other words, Great Innovation paid $12.5 for each share of Series Seed Preferred stock.

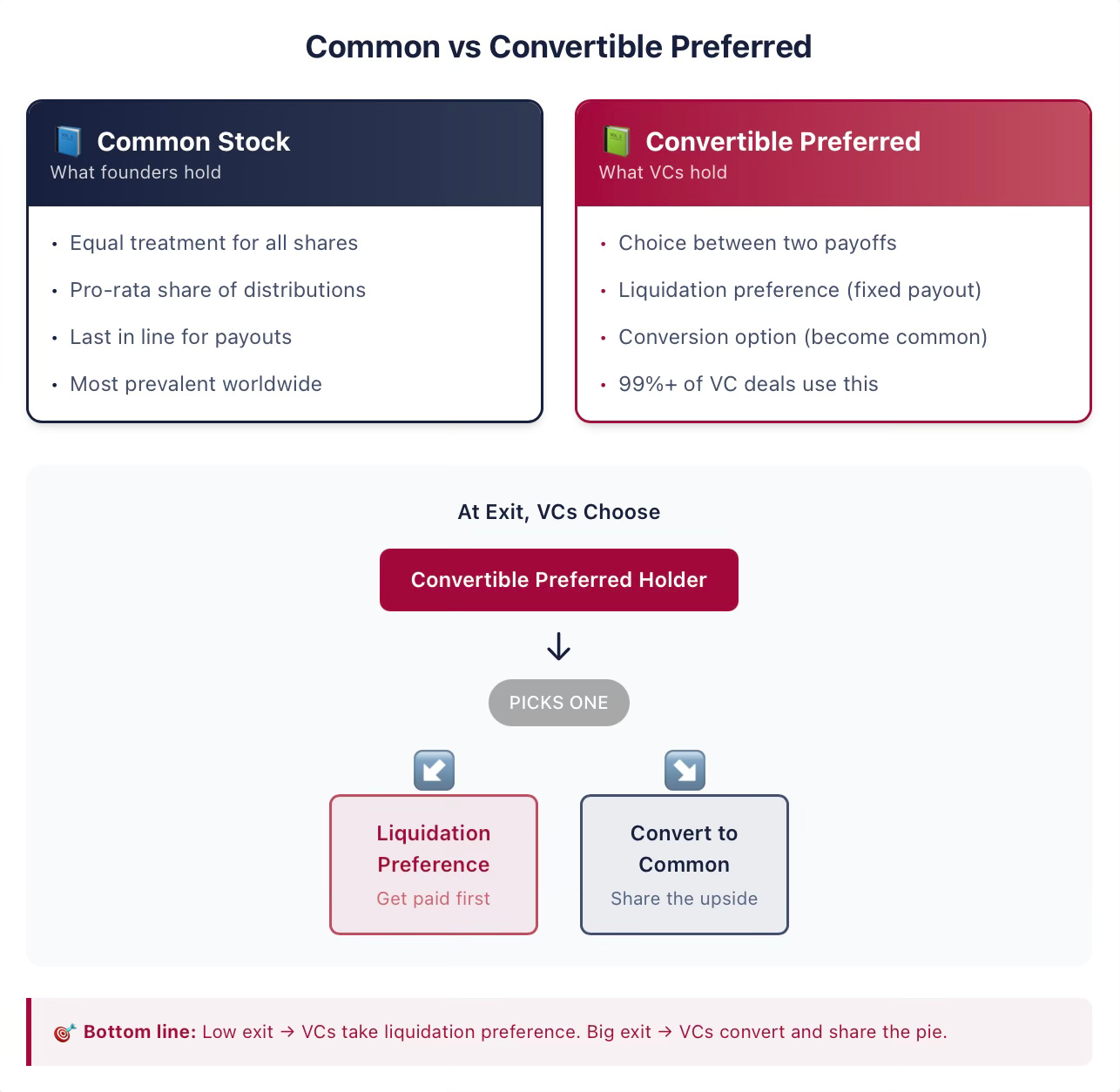

Founders Typically Own Common Stock

Founders of early-stage companies typically own common stock, the most prevalent type of ownership in public and private companies around the world.1 Stock is a form of corporate ownership that entitles its owners (known as stockholders) to certain rights. In other words, stockholders have a claim on the company. Equity is another term that is often used to describe stock claim, and we will use stock and equity interchangeably here. The words “stock” or “equity” also distinguish these securities from another often-used type of corporate claim, debt.2

The addition of “common” in “common stock” or “common equity” really takes on meaning if there are other types of securities issued by the same company. If common stock is the only security issued by the company, then each company share is treated equally to any other company share – there is only one type of claim outstanding! More generally, each common share is treated in the same way as any other common share.

When there’s a payout, one common share is entitled to exactly the same payoff as any other common share. The payoff is thus divided equally among all the outstanding common shares. However, if other owners have a security of another type, the payoff could be divided very differently. In VC transactions, this is almost always the case.

Investors Own Convertible Preferred Stock

Series A Preferred stock that Top Gun acquires is an example of convertible preferred stock. Convertible preferred stock is the security of choice for most VC investors in the U.S. This security combines features of both debt and common equity. Unfortunately for aspiring entrepreneurs or start-up investors, this security offers a complicated structure, especially when compared to straight debt and common equity – traditional financial securities. Fortunately, we will now master it together.

At its core, convertible preferred stock is a financial security that gives its owner the right to choose between two possible payoff options. The owner can choose to convert the convertible preferred stock into a different security, typically into common equity (this is called the optional conversion feature). Or, the owner can get a lump-sum payout before common equityholders get anything (this is called the liquidation preference feature). This right is usually subject to many caveats and depends on many additional contractual provisions that we will be exploring. But the core idea is that the security provides investors with the choice between the conversion feature and the liquidation preference feature.

It is very important to note – especially to those who have experience in stock markets and investment banking – that in traditional financial markets companies also, from time to time, may issue securities that are known as preferred stock. While superficially similar, the securities issued in VC transactions have a number of features that stand them way apart. If you know preferred stock from public markets — this is different. Don’t skip this.

Example 2. Preferred Stock Issued by a Public Company

In 2018, MetLife, a large public insurance company, issued a new series of preferred stock, MET-E, offering 28 million shares to the market. Preferred stock of this kind functions similarly to a debt security, with investors guaranteed a fixed dividend payment in perpetuity. MET-E offers investors a 5.63% coupon but does not offer any voting rights (unlike common stock). Holders of preferred stock have priority over the company’s income and are paid dividends before common shareholders (but after debtholders). Preferred stock like MET-E generally does not have conversion features.

VC contracts typically call this security Preferred stock, but when you see Preferred stock in a VC contract or a term sheet, you can safely assume it is also convertible. In my analysis of thousands of VC contracts, more than 99% of ‘Preferred stock’ is actually convertible.

While contracts often omit “Convertible” in the security name, they usually have other add-ons. For example, the security may be named Series A Preferred stock, as in the case of Top Gun’s proposed investment.

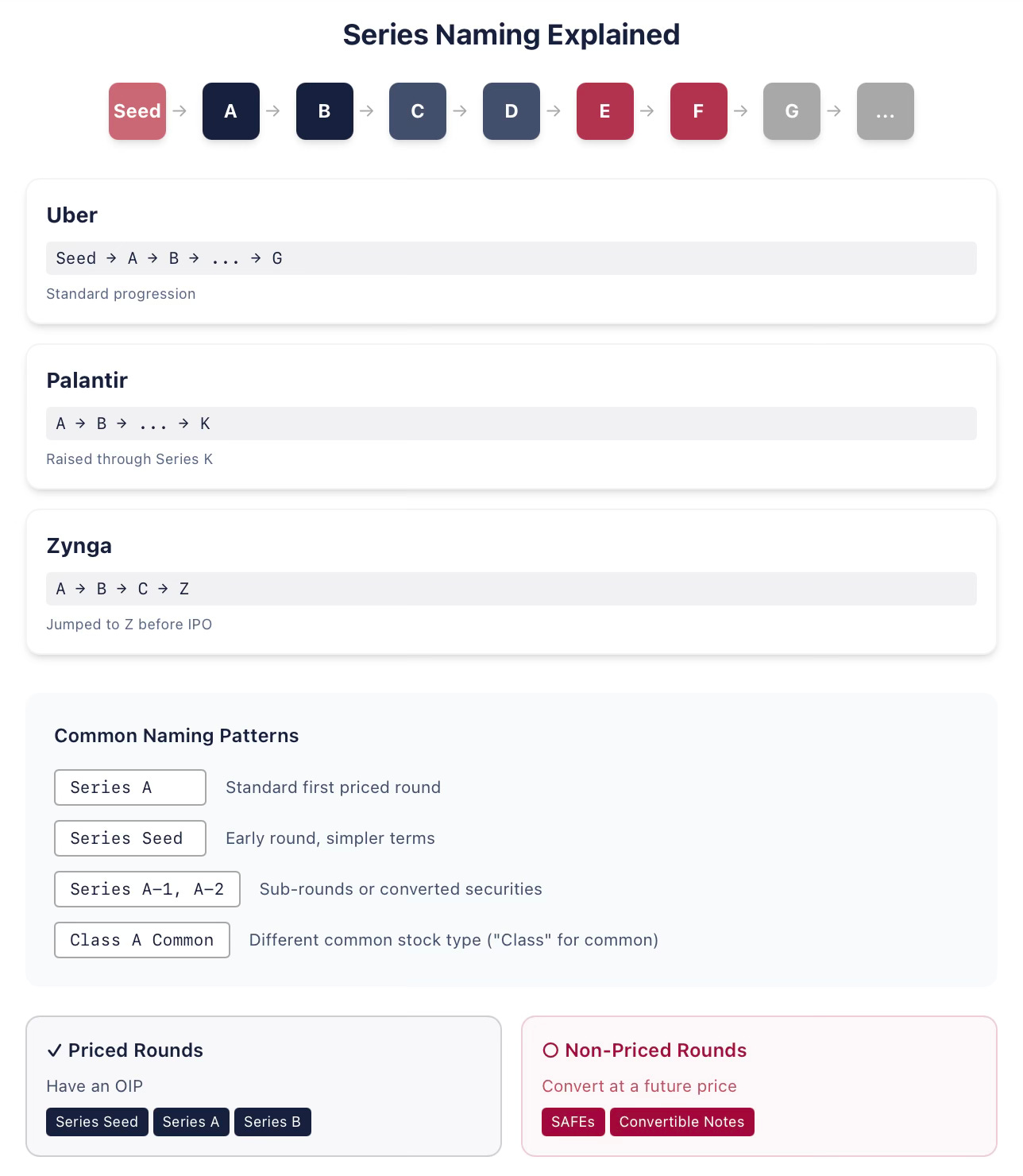

Example 3. Letters in Series

Ride-sharing company Uber issued Series Seed, Series A, Series B, and so on, through to Series G Preferred stock during its time as a private VC-backed company. Big data analytics company Palantir issued Series K Preferred stock in its 2015 financing round (previously having issued Series A to Series J). Space company SpaceX just may run out oi letters of alphabet for naming its series of preferred stock before it eventually goes public (I am writing this in January of 2026). Sometimes, companies issue securities out of alphabetical order, as when the company is undergoing reorganization. For example, online-gaming company Zynga issued Series A, Series B, and Series C Preferred stock, and then jumped to Series Z Preferred stock prior to its initial public offering.

Historically, Series A Preferred stock was the name given to the security issued in the first VC financing round. In the last fifteen years or so, the first security is also often called Series Seed Preferred Stock (as in the case of Uber). This often signals that this security may have simpler structure than the fully-fledged Series A Preferred stock. Founders and investors also may want to send a message that this is a very early-stage company. Once the company raises another financing round, it will then typically issue Series A Preferred stock. The implication is that you should not assume that “Series A” necessarily means first VC round.

What then is the first VC round? The best way to ask whether this round is a priced round, that is whether the security has OIP. If the company issues SAFE or a convertible note, it is not a priced round, but Series Seed Preferred stock is a priced round. (Be careful: what you typically hear is that non-priced rounds do not put any valuation on the company. This is not correct, as we will discuss in due time.)

Lawyers advising VC investors and startups are quite creative in naming stuff, so there are many other variations on the naming possibilities. Sometimes these subtle name differences signify some specific arrangements. For instance, any series could also be followed or accompanied by additional numbered series (Series A may be followed by Series A-1, A-2, etc.). If a part of the same round, usually such Series A-1 stocks differ only slightly in some specific terms and are otherwise identical to Series A, often because of conversion of some outstanding securities into (almost) Series A. Alternatively, they could be a part of a completely different financing round, for example, because the company does not yet feel it reached the milestones that the market expects for Series B companies in this space.

Convertible preferred stock is by far the most common financial contract VC investors use in early-stage startup financing in the U.S. In a sample of more than 1,500 investment rounds by more than 500 U.S. VC-backed companies that took place between 1995 and 2025, almost every single equity financing included convertible preferred stock or one of its many variants.4 Taking a look at the most valued VC-backed companies, unicorns, we see that every single one of them used this type of financial security at least once, and most of them have used it in almost all of their rounds of financing.5 This is not a recent phenomenon. For a sample of about 200 financing rounds at an earlier period of the 1990s, about 95% involved convertible preferred stock, sometimes in conjunction with other securities.6

Why this peculiar structure? It’s a deep question — and one we’ll explore in a future article. For now, let’s focus on what it means for payoffs.

Key Takeaways

The relationship between Original issue price (OIP), investment amount, and the number of shares that investor receives determines investor ownership.

Two most common types of securities that early-stage companies issue are common stock and convertible preferred stock.

Convertible preferred stock owners get payoff through conversion and/or liquidation preference.

If you see security price or post-money valuation given, it is a priced round.

Hi Ilya! I hope you’re doing well. I have studied some of these topics previously and found a good refresher in your article. The article explains the basics of VC very simply and shortly.

I write a newsletter in substack titled “The LegalTech Thesis” wherein I analyze LegalTech startups and identify investment opportunities in the space. Would love to get your thoughts on my post analyzing the three big whitespaces in 2026 for LegalTech!

Grateful for the initiative, please keep them coming